Top Tax-Saving Investments Under Section 80C for FY 2024-25 | Best Options for Maximum Savings

-

- by MI September 22, 2025

When it comes to reducing your income tax liability, Section 80C of the Income Tax Act is the most widely used option by salaried employees and taxpayers in India. For FY 2024-25 (AY 2025-26), the maximum deduction allowed under Section 80C remains ₹1.5 lakh. By choosing the right mix of investments, you can save tax while also building long-term wealth.

In this blog, we’ll explore the best tax-saving investments under Section 80C for FY 2024-25.

1. Public Provident Fund (PPF)

- Long-term investment with a lock-in of 15 years.

- Current interest rate: ~7.1% (tax-free).

- Safe and government-backed.

2. Employees’ Provident Fund (EPF)

- Mandatory contribution for salaried employees.

- Employer contribution is also eligible in some cases.

- Interest and maturity proceeds are tax-free (EEE status).

3. Equity Linked Savings Scheme (ELSS)

- Mutual funds with 3-year lock-in (lowest among 80C options).

- Potentially higher returns as it invests in equities.

- Eligible for deduction up to ₹1.5 lakh.

4. Life Insurance Premiums

- Premiums paid for life insurance policies qualify under 80C.

- Available for policies for self, spouse, and children.

- Good for financial protection + tax benefit.

5. National Savings Certificate (NSC)

- Fixed-income investment with a 5-year lock-in.

- Interest is taxable but qualifies again under 80C.

- Safe option for conservative investors.

6. Sukanya Samriddhi Yojana (SSY)

- Scheme for a girl child’s education and marriage.

- High interest rate (~8%) and exempt at maturity.

- Parents/guardians can deposit up to ₹1.5 lakh annually.

7. 5-Year Tax-Saving Fixed Deposits

- Minimum lock-in of 5 years.

- Interest is taxable.

- Suitable for risk-averse investors.

Comparison: Safe vs Growth-Oriented 80C Investments

| Investment Option | Category | Lock-in Period | Expected Returns | Risk Level |

|---|---|---|---|---|

| Public Provident Fund (PPF) | Safe | 15 years | ~7.1% (tax-free) | Low |

| Employees’ Provident Fund (EPF) | Safe | Until retirement | ~8% (tax-free) | Low |

| National Savings Certificate (NSC) | Safe | 5 years | ~7% (taxable) | Low |

| Sukanya Samriddhi Yojana (SSY) | Safe | Until girl turns 21 years | ~8% (tax-free) | Low |

| Tax-Saving Fixed Deposit | Safe | 5 years | ~6-7% (taxable) | Low |

| Equity Linked Savings Scheme (ELSS) | Growth | 3 years | 12-15% (market-linked) | High |

| Life Insurance Premium | Safe + Protection | Depends on policy term | Low to Moderate | Low |

Conclusion

Section 80C offers multiple avenues for tax-saving and wealth creation. Salaried employees should balance between safe instruments (PPF, EPF, NSC) and growth-oriented investments (ELSS) to optimize both returns and tax benefits.

By investing smartly, you can claim the full ₹1.5 lakh deduction under 80C and significantly lower your tax outgo in FY 2024-25.

See More Related Blog

Aadhaar and Income Tax: Linking PAN and Filing ITR in 2025

-

- by MI

In 2025, linking your Aadhaar card with PAN is mandatory for filing Income Tax Returns (ITR) in India. Aadhaar-PAN linking ensures seamless verification, reduces tax…

Section 54: How to Save Capital Gains Tax on Property Sales in 2025

-

- by MI

Selling a property in India can attract long-term capital gains tax (LTCG) if held for more than 24 months (residential property). However, under Section 54 of the…

Advance Tax vs Self-Assessment Tax: Key Differences Explained

-

- by MI

Many taxpayers in India get confused between Advance Tax and Self-Assessment Tax. While both involve paying taxes directly to the government, they differ in terms of…

How to File Income Tax for Senior Citizens in 2025

-

- by MI

Senior citizens (60 years and above) enjoy higher exemption limits and special deductions while filing income tax in India. This guide explains, step by step, how senior…

How to Claim Home Loan Tax Benefits under Section 24(b) and 80C in 2025

-

- by MI

Buying a home is one of the biggest financial decisions in India, and the government provides multiple tax benefits on home loans to reduce the burden on taxpayers.…

Agricultural Income and Taxation Rules in India 2025

-

- by MI

Agriculture continues to be a backbone of the Indian economy, and the government provides special income tax exemptions to support farmers. However, agricultural income…

Impact of GST 2.0 on Income Tax Collections in India: 2025 Analysis

-

- by MI

The implementation of GST 2.0 in India marks a significant step towards tax simplification and improved compliance. While GST primarily affects indirect taxation, it…

Section 87A Rebate: Eligibility and Tax Savings in 2025

-

- by MI

Section 87A of the Income Tax Act provides a tax rebate for resident individuals with income below a certain threshold. Understanding eligibility, rebate amount, and tax…

House Property and Rental Income: Taxation Rules in 2025

-

- by MI

Rental income from house property is a common source of income in India. Understanding how house property income is taxed, deductions allowed, and filing rules is…

How NRI Income Tax Rules Work in India: 2025 Guide

-

- by MI

Non-Resident Indians (NRIs) have unique tax obligations in India. Understanding NRI income tax rules, exemptions, and filing requirements is crucial to stay compliant in…

Capital Gains Tax in India 2025: Short-Term vs Long-Term Explained

-

- by MI

Capital gains tax is a crucial part of India’s income tax system. Whether you are an investor in stocks, mutual funds, or real estate, understanding the difference…

Advance Tax Payment in India: Due Dates, Calculation & Penalties 2025 Guide

-

- by MI

Advance Tax is a system where taxpayers pay their tax liability in installments instead of a lump sum at the end of the financial year. This ensures timely collection of…

How Freelancers and Gig Workers Can Save Tax in India: 2025 Step-by-Step Guide

-

- by MI

Freelancers and gig economy workers are a rapidly growing part of India’s workforce. While this offers flexibility and higher earning potential, tax compliance can be…

TDS (Tax Deducted at Source) Explained: Rules, Rates & Latest Changes 2025

-

- by MI

Tax Deducted at Source (TDS) is a key part of India’s taxation system. It ensures tax is collected directly from the source of income, preventing evasion and improving…

Complete Guide to Income Tax Deductions and Exemptions in 2025

-

- by MI

This guide explains the most important deductions and exemptions available to taxpayers in India in 2025 (FY 2024–25 / AY 2025–26), how to claim them step-by-step,…

Income Tax on Salaried Employees: Deductions, Rebates, and Exemptions 2025

-

- by MI

The financial year 2024–25 (Assessment Year 2025–26) brings several important updates for salaried employees in India. With reforms in the Income Tax Act, choosing…

Step-by-Step Guide to Filing Income Tax Returns (ITR) Online in 2025

-

- by MI

Filing your Income Tax Return (ITR) online has become easier than ever in 2025, thanks to digital initiatives by the Income Tax Department. The process is completely…

Old vs New Tax Regime 2025: Which One Should You Choose?

-

- by MI

With the government continuing to promote the new tax regime in 2025 as the default option, taxpayers are left with an important question – Old vs New Tax Regime: Which…

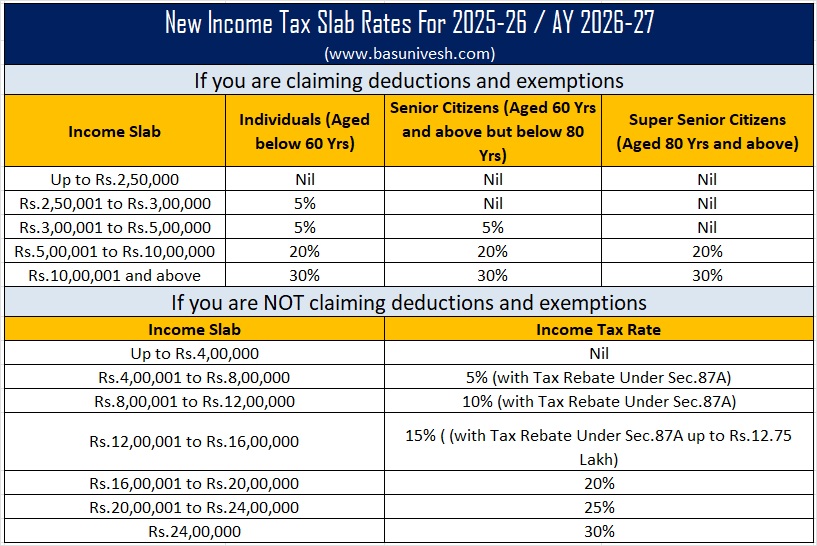

Income Tax Slabs in India 2025: Latest Updates and Comparison with 2024

-

- by MI

The Indian government announces Income Tax Slabs every year during the Union Budget. For FY 2025–26, the government has retained the focus on the new simplified tax…

Comments

Add new comment