Complete Guide to Income Tax Deductions and Exemptions in 2025

-

- by MI September 22, 2025

This guide explains the most important deductions and exemptions available to taxpayers in India in 2025 (FY 2024–25 / AY 2025–26), how to claim them step-by-step, required documents, and common pitfalls to avoid.

Quick orientation

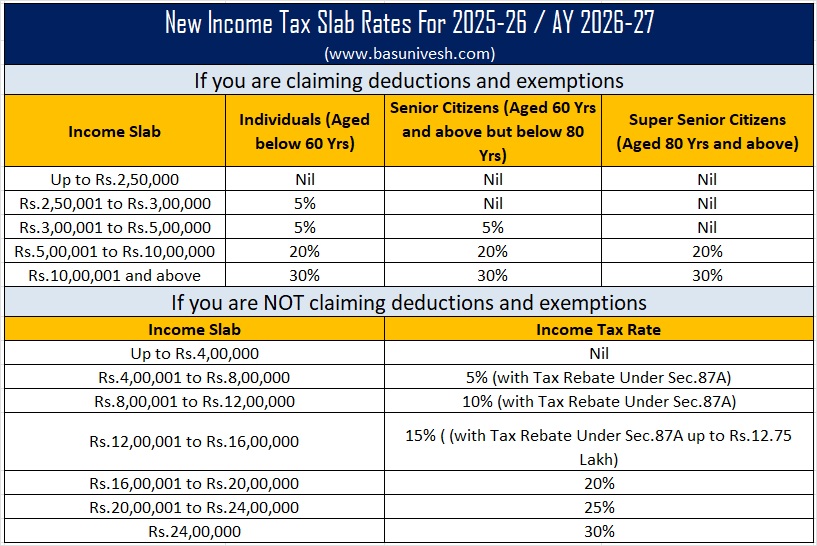

- Old vs New tax regime: Many popular deductions (eg. most Section 80 benefits) are available under the old regime. The new regime offers lower slab rates but fewer deductions — check both before you file.

- Standard deduction & rebate changes (2025): there were key changes in 2025 (standard deduction availability and rebate thresholds) — confirm items below when planning. (See sources at the end.)

STEP 1 — Decide your tax regime (Old vs New)

- List your expected deductions for the year (80C, 80D, home loan interest, HRA, etc.).

- Compute approximate tax under both regimes (taxable income after deductions vs new-regime slabs).

- Choose the regime that gives lower tax for your situation — you can switch each year subject to rules. If unsure, run quick comparisons with a calculator or ask your tax advisor.

STEP 2 — Know the cornerstone, standard deduction & rebate

Standard deduction: salaried taxpayers get a standard deduction (check current amount and whether the new regime allows it). Also check the Section 87A rebate thresholds for the year you’re filing — these change with the Budget. (Official FAQ and Budget doc confirm the 2025 changes listed in sources.)

STEP 3 — Table: Key Deductions & Exemptions (what, limit, notes, docs)

| Section | What it covers | Limit (typical / FY 2024-25) | Notes & Documents |

|---|---|---|---|

| Section 80C | PPF, ELSS, EPF, life insurance premiums, principal repayment of home loan, SSY, NSC, tuition fees | Up to ₹1,50,000 total per year. :contentReference[oaicite:0]{index=0} | Provide investment receipts, policy/account numbers, PPF passbook screenshots, mutual fund statements. |

| Section 80CCD(1B) | Additional self-contribution to NPS (Tier I) | Up to ₹50,000 (over & above 80C limit). :contentReference[oaicite:1]{index=1} | Use NPS contribution statement; quote PRAN/account number. |

| Section 80D | Health insurance premium / preventive health check-up | Up to ₹25,000 for self & family; higher limits apply for senior citizens (check current limits). :contentReference[oaicite:2]{index=2} | Insurance premium receipt, policy number, GST invoice for premium. |

| Section 24(b) | Interest on home loan (Income from house property) | Up to ₹2,00,000 for self-occupied property (old regime / where applicable). :contentReference[oaicite:3]{index=3} | Loan interest certificate from lender, principal & interest breakup. |

| House Rent Allowance (HRA) — Sec 10(13A) | Exemption for rent paid (if you receive HRA) | Exemption = least of (a) HRA received; (b) rent paid − 10% of salary; (c) 50% of salary (metro) or 40% (non-metro). :contentReference[oaicite:4]{index=4} | Rent receipts / lease agreement, landlord PAN (if rent >₹1L/yr), Form 12BB details to employer. |

| Section 80E | Interest on education loan | No upper monetary limit; allowable for loan tenure (specified years) | Loan account statement, interest certificate from lender. |

| Section 80G | Donations to eligible charities | Varies — some donations 50% or 100% of donation with/without restriction | Donation receipt with PAN of donee, registration/80G certificate. |

| Section 80TTA / 80TTB | Interest on savings bank deposits / interest on deposits for seniors | 80TTA: up to ₹10,000 (non-senior); 80TTB: up to ₹50,000 (senior citizens). :contentReference[oaicite:5]{index=5} | Bank interest statement (Form 16A / bank statement). |

| Gratuity / Leave Encashment / PF | Certain service-related receipts are exempt up to statutory limits | Limits vary by rules (gratuity ceiling, PF exemption rules) | Service record, employer certificate, PF statement. |

Notes: some deductions (eg. most 80C items, 24(b) home loan interest) are typically claimed under the old regime. The new regime in 2025 includes some changes — check the Budget/Income Tax FAQ to see which deductions remain available (key official FAQ listed below).

STEP 4 — Step-by-step: How to claim these deductions (practical)

- Start early: compile receipts / account numbers through the year (mutual fund folios, PPF passbook, premium receipts).

- Tell your employer (Form 12BB): submit proof of investments and HRA/rent details so TDS is deducted correctly during the year (reduces TDS and improves cashflow). Employers usually require these proofs annually.

- Collect lender/insurer certificates: lender interest certificates, insurance premium receipts, NPS contribution slips, donation receipts with registration numbers.

- Enter details in ITR: use the ITR utility (income tax e-filing) to fill schedules for deductions — schedule-wise fields exist (eg. Schedule VIA for certain deductions; house property schedule for 24(b)).

- Attach supporting info when requested: the new ITR utility may ask for policy/folio numbers, landlord details, etc. Save scanned copies.

- Submit & e-verify: file, e-verify via Aadhaar OTP / netbanking / DSC to complete filing.

STEP 5 — Documentation checklist (what to keep)

- Investment receipts & account numbers (PPF, ELSS, PPF passbook pages)

- Life insurance premium receipts, policy numbers

- Health insurance premium receipts, policy number & insurer name

- Loan interest certificate & principal repayment schedule from bank

- Rent receipts / lease agreement / landlord PAN (if required)

- Donation receipts with registration number for 80G

- Form 16, Form 26AS / AIS (Annual Information Statement)

STEP 6 — Common mistakes & how to avoid them

- Claiming a deduction without supporting documents — keep originals and scanned copies.

- Double-counting the same investment across sections (e.g., both 80C and elsewhere).

- Not submitting Form 12BB to employer — leads to higher TDS.

- Ignoring special-rate incomes (STCG/LTCG) that may not be eligible for certain rebates — understand exclusions.

STEP 7 — Small employer / freelancer tips

- Self-employed: claim deductions while filing ITR (there’s no Form 12BB route for reducing TDS).

- Freelancers/contractors: maintain invoices and bank transaction proofs to tie income & expenses.

Useful examples (how to think about deduction stacking)

- Max out 80C (₹1.5L) first if you have long-term commitments (PPF/ELSS/EPF/principal repayment).

- Top up NPS under 80CCD(1B) for an extra ₹50k benefit (if retirement saving is ok for you).

- Buy or maintain adequate family health cover to utilize 80D limits (helps both protection and tax).

- If you pay rent, estimate HRA exemption — sometimes it saves more than investing in 80C instruments.

FAQ — short answers

- Can I claim 80C + 80CCD(1B)? Yes — 80C aggregate limit is ₹1.5L, plus 80CCD(1B) allows an additional ₹50k (NPS), subject to rules. :contentReference[oaicite:6]{index=6}

- Is health insurance premium deductible? Yes — within limits (80D). Keep premium receipts and policy numbers. :contentReference[oaicite:7]{index=7}

- Is home loan interest deductible? Interest on self-occupied property is generally allowed up to ₹2L under Section 24(b) (subject to rules); check whether you’re filing old or new regime. :contentReference[oaicite:8]{index=8}

- Where do I enter these in ITR? Deductions go into Schedule VIA / specific schedules for house property / other sections when you use the e-filing utility.

Quick checklist before you file:

- Collect receipts and lender/insurer certificates.

- Submit Form 12BB to employer (if salaried).

- Reconcile Form 26AS / AIS with your Form 16 and bank statements.

- File ITR, attach/enter required details, and e-verify within 30 days.

Need-to-know legal / authoritative references

Check the official Income Tax Department FAQ and your Budget notes for authoritative confirmation of slab/rebate and standard deduction changes in 2025 — details and exact numeric thresholds are published by the government each Budget and in the Income Tax Department FAQs (links in sources below).

If you want, I can also:

- Convert this into a one-page downloadable PDF for readers.

- Create a small deduction calculator (HTML + JS) to help readers estimate taxable income after deductions.

See More Related Blog

Aadhaar and Income Tax: Linking PAN and Filing ITR in 2025

-

- by MI

In 2025, linking your Aadhaar card with PAN is mandatory for filing Income Tax Returns (ITR) in India. Aadhaar-PAN linking ensures seamless verification, reduces tax…

Section 54: How to Save Capital Gains Tax on Property Sales in 2025

-

- by MI

Selling a property in India can attract long-term capital gains tax (LTCG) if held for more than 24 months (residential property). However, under Section 54 of the…

Advance Tax vs Self-Assessment Tax: Key Differences Explained

-

- by MI

Many taxpayers in India get confused between Advance Tax and Self-Assessment Tax. While both involve paying taxes directly to the government, they differ in terms of…

How to File Income Tax for Senior Citizens in 2025

-

- by MI

Senior citizens (60 years and above) enjoy higher exemption limits and special deductions while filing income tax in India. This guide explains, step by step, how senior…

How to Claim Home Loan Tax Benefits under Section 24(b) and 80C in 2025

-

- by MI

Buying a home is one of the biggest financial decisions in India, and the government provides multiple tax benefits on home loans to reduce the burden on taxpayers.…

Agricultural Income and Taxation Rules in India 2025

-

- by MI

Agriculture continues to be a backbone of the Indian economy, and the government provides special income tax exemptions to support farmers. However, agricultural income…

Impact of GST 2.0 on Income Tax Collections in India: 2025 Analysis

-

- by MI

The implementation of GST 2.0 in India marks a significant step towards tax simplification and improved compliance. While GST primarily affects indirect taxation, it…

Section 87A Rebate: Eligibility and Tax Savings in 2025

-

- by MI

Section 87A of the Income Tax Act provides a tax rebate for resident individuals with income below a certain threshold. Understanding eligibility, rebate amount, and tax…

House Property and Rental Income: Taxation Rules in 2025

-

- by MI

Rental income from house property is a common source of income in India. Understanding how house property income is taxed, deductions allowed, and filing rules is…

How NRI Income Tax Rules Work in India: 2025 Guide

-

- by MI

Non-Resident Indians (NRIs) have unique tax obligations in India. Understanding NRI income tax rules, exemptions, and filing requirements is crucial to stay compliant in…

Capital Gains Tax in India 2025: Short-Term vs Long-Term Explained

-

- by MI

Capital gains tax is a crucial part of India’s income tax system. Whether you are an investor in stocks, mutual funds, or real estate, understanding the difference…

Advance Tax Payment in India: Due Dates, Calculation & Penalties 2025 Guide

-

- by MI

Advance Tax is a system where taxpayers pay their tax liability in installments instead of a lump sum at the end of the financial year. This ensures timely collection of…

How Freelancers and Gig Workers Can Save Tax in India: 2025 Step-by-Step Guide

-

- by MI

Freelancers and gig economy workers are a rapidly growing part of India’s workforce. While this offers flexibility and higher earning potential, tax compliance can be…

TDS (Tax Deducted at Source) Explained: Rules, Rates & Latest Changes 2025

-

- by MI

Tax Deducted at Source (TDS) is a key part of India’s taxation system. It ensures tax is collected directly from the source of income, preventing evasion and improving…

Top Tax-Saving Investments Under Section 80C for FY 2024-25 | Best Options for Maximum Savings

-

- by MI

When it comes to reducing your income tax liability, Section 80C of the Income Tax Act is the most widely used option by salaried employees and taxpayers in India. For…

Income Tax on Salaried Employees: Deductions, Rebates, and Exemptions 2025

-

- by MI

The financial year 2024–25 (Assessment Year 2025–26) brings several important updates for salaried employees in India. With reforms in the Income Tax Act, choosing…

Step-by-Step Guide to Filing Income Tax Returns (ITR) Online in 2025

-

- by MI

Filing your Income Tax Return (ITR) online has become easier than ever in 2025, thanks to digital initiatives by the Income Tax Department. The process is completely…

Old vs New Tax Regime 2025: Which One Should You Choose?

-

- by MI

With the government continuing to promote the new tax regime in 2025 as the default option, taxpayers are left with an important question – Old vs New Tax Regime: Which…

Income Tax Slabs in India 2025: Latest Updates and Comparison with 2024

-

- by MI

The Indian government announces Income Tax Slabs every year during the Union Budget. For FY 2025–26, the government has retained the focus on the new simplified tax…

Comments

Add new comment