Section 54: How to Save Capital Gains Tax on Property Sales in 2025

-

- by MI September 22, 2025

Selling a property in India can trigger long-term capital gains (LTCG) tax if the asset is held for more than 24 months. However, under Section 54 of the Income Tax Act, individuals and Hindu Undivided Families (HUFs) can save or reduce their capital gains tax by reinvesting the sale proceeds in a residential property. This detailed guide explains the rules, timelines, calculations, and tips for saving capital gains tax in 2025.

1. What is Section 54?

Section 54 allows exemption from LTCG tax on the sale of a residential property when the gains are reinvested in purchasing or constructing another residential property in India.

Eligibility Criteria

- Capital gains must be long-term (property held for more than 24 months).

- Exemption is available only for residential properties.

- Reinvestment must be completed within prescribed timelines.

- Applicable for individuals and HUFs.

2. How Reinvestment Works

You can save capital gains tax by either:

- Purchasing a new residential property within 1 year before or 2 years after selling the old property.

- Constructing a new residential property within 3 years from the date of sale.

It is essential to ensure the new property is only in your name (or jointly, in some cases) and proper documentation is maintained.

3. Calculating Exemption Under Section 54

The exemption is limited to the capital gains or the cost of the new property, whichever is lower. Any unutilized capital gains must be deposited in the Capital Gains Account Scheme (CGAS) before filing your Income Tax Return (ITR).

Step-by-Step Calculation

- Compute Long-Term Capital Gains (LTCG):

LTCG = Sale Price of Old Property − Indexed Cost of Acquisition − Indexed Cost of Improvements - Determine purchase/construction cost of the new residential property.

- Exemption under Section 54 = Minimum of LTCG or cost of new property.

- Any remaining LTCG after exemption is taxable.

4. Example

Suppose you sell a house in 2025 for ₹80 lakh, and the indexed cost of acquisition is ₹50 lakh. LTCG = ₹30 lakh.

You purchase a new residential property for ₹28 lakh within 2 years. Exemption = ₹28 lakh. Taxable LTCG = ₹30 lakh − ₹28 lakh = ₹2 lakh.

5. Important Timelines

| Action | Timeline |

|---|---|

| Purchase new residential property | Within 1 year before or 2 years after sale |

| Construct new residential property | Within 3 years from sale |

| Deposit unutilized gains in CGAS | Before filing ITR |

6. Section 54F: Slightly Different Rules

If the original asset sold is other than a residential property (like land or commercial property), Section 54F applies. You can still claim exemption if you invest in a residential property, but only one property can be claimed per taxpayer.

7. Key Points to Remember

- If the new property is sold within 3 years, the exemption claimed earlier will be reversed.

- Keep all sale and purchase documents safely for ITR filing and possible scrutiny.

- Section 54 exemption is available only once for one residential property.

- CGAS is mandatory if the reinvestment is not made before ITR filing.

8. Practical Tips for 2025

- Plan the property purchase in advance to ensure compliance with Section 54 timelines.

- Consult a CA to correctly calculate indexed cost and exemptions.

- Keep all bank statements and sale/purchase agreements ready for documentation.

- Consider Section 54F if selling a commercial property and planning to invest in residential property.

Conclusion

Section 54 provides a significant opportunity to save capital gains tax when selling a residential property. By understanding eligibility, timelines, and reinvestment rules, taxpayers in 2025 can legally minimize their LTCG liability. Proper planning and documentation are key to making the most of this exemption.

See More Related Blog

Aadhaar and Income Tax: Linking PAN and Filing ITR in 2025

-

- by MI

In 2025, linking your Aadhaar card with PAN is mandatory for filing Income Tax Returns (ITR) in India. Aadhaar-PAN linking ensures seamless verification, reduces tax…

Advance Tax vs Self-Assessment Tax: Key Differences Explained

-

- by MI

Many taxpayers in India get confused between Advance Tax and Self-Assessment Tax. While both involve paying taxes directly to the government, they differ in terms of…

How to File Income Tax for Senior Citizens in 2025

-

- by MI

Senior citizens (60 years and above) enjoy higher exemption limits and special deductions while filing income tax in India. This guide explains, step by step, how senior…

How to Claim Home Loan Tax Benefits under Section 24(b) and 80C in 2025

-

- by MI

Buying a home is one of the biggest financial decisions in India, and the government provides multiple tax benefits on home loans to reduce the burden on taxpayers.…

Agricultural Income and Taxation Rules in India 2025

-

- by MI

Agriculture continues to be a backbone of the Indian economy, and the government provides special income tax exemptions to support farmers. However, agricultural income…

Impact of GST 2.0 on Income Tax Collections in India: 2025 Analysis

-

- by MI

The implementation of GST 2.0 in India marks a significant step towards tax simplification and improved compliance. While GST primarily affects indirect taxation, it…

Section 87A Rebate: Eligibility and Tax Savings in 2025

-

- by MI

Section 87A of the Income Tax Act provides a tax rebate for resident individuals with income below a certain threshold. Understanding eligibility, rebate amount, and tax…

House Property and Rental Income: Taxation Rules in 2025

-

- by MI

Rental income from house property is a common source of income in India. Understanding how house property income is taxed, deductions allowed, and filing rules is…

How NRI Income Tax Rules Work in India: 2025 Guide

-

- by MI

Non-Resident Indians (NRIs) have unique tax obligations in India. Understanding NRI income tax rules, exemptions, and filing requirements is crucial to stay compliant in…

Capital Gains Tax in India 2025: Short-Term vs Long-Term Explained

-

- by MI

Capital gains tax is a crucial part of India’s income tax system. Whether you are an investor in stocks, mutual funds, or real estate, understanding the difference…

Advance Tax Payment in India: Due Dates, Calculation & Penalties 2025 Guide

-

- by MI

Advance Tax is a system where taxpayers pay their tax liability in installments instead of a lump sum at the end of the financial year. This ensures timely collection of…

How Freelancers and Gig Workers Can Save Tax in India: 2025 Step-by-Step Guide

-

- by MI

Freelancers and gig economy workers are a rapidly growing part of India’s workforce. While this offers flexibility and higher earning potential, tax compliance can be…

TDS (Tax Deducted at Source) Explained: Rules, Rates & Latest Changes 2025

-

- by MI

Tax Deducted at Source (TDS) is a key part of India’s taxation system. It ensures tax is collected directly from the source of income, preventing evasion and improving…

Complete Guide to Income Tax Deductions and Exemptions in 2025

-

- by MI

This guide explains the most important deductions and exemptions available to taxpayers in India in 2025 (FY 2024–25 / AY 2025–26), how to claim them step-by-step,…

Top Tax-Saving Investments Under Section 80C for FY 2024-25 | Best Options for Maximum Savings

-

- by MI

When it comes to reducing your income tax liability, Section 80C of the Income Tax Act is the most widely used option by salaried employees and taxpayers in India. For…

Income Tax on Salaried Employees: Deductions, Rebates, and Exemptions 2025

-

- by MI

The financial year 2024–25 (Assessment Year 2025–26) brings several important updates for salaried employees in India. With reforms in the Income Tax Act, choosing…

Step-by-Step Guide to Filing Income Tax Returns (ITR) Online in 2025

-

- by MI

Filing your Income Tax Return (ITR) online has become easier than ever in 2025, thanks to digital initiatives by the Income Tax Department. The process is completely…

Old vs New Tax Regime 2025: Which One Should You Choose?

-

- by MI

With the government continuing to promote the new tax regime in 2025 as the default option, taxpayers are left with an important question – Old vs New Tax Regime: Which…

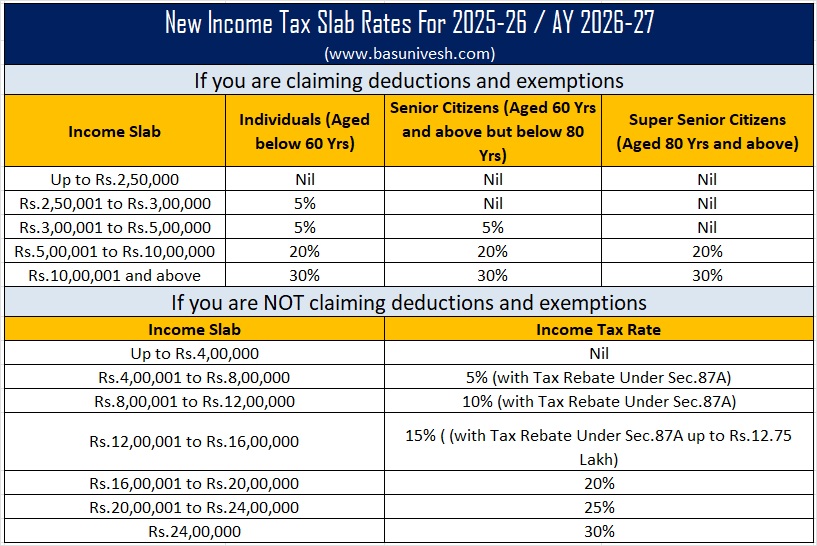

Income Tax Slabs in India 2025: Latest Updates and Comparison with 2024

-

- by MI

The Indian government announces Income Tax Slabs every year during the Union Budget. For FY 2025–26, the government has retained the focus on the new simplified tax…

Comments

Add new comment